Book 3. Financial Markets and Products

FRM Part 1

FMP 9. Foreign Exchange Markets

Presented by: Sudhanshu

Module 1. Foreign Exchange Quotes and Risks

Module 2. Interest Rates, Inflation and Exchange Rates

Module 1. Foreign Exchange Quotes and Risks

Topic 1. Spot, Forward, and Futures Quotes

Topic 2. Outright (Forward) and Swap Transactions

Topic 3. Transaction, Translation, and Economic Risk

Topic 4. Multicurrency Hedging

Topic 1. Spot, Forward, and Futures Quotes

-

Spot Quote: Immediate exchange rate; 4 decimal places.

-

Example: CADUSD Bid 0.7535 / Ask 0.7541 → Spread = 0.0006

-

-

Forward Quote: Future rate, quoted in points added/subtracted from spot.

-

E.g., 3M Forward Points: Bid 90.11 → Forward Bid = 0.7535 + 0.009011 = 0.762511

-

-

Futures Quote: Uses USD as quote currency (XXXUSD), often inverse of forward.

Practice Questions: Q1

Q1. Assume the GBPUSD spot quote is bid 1.2944 and ask 1.2952. The three-month forward points quote is bid 56.34 and ask 58.85. The forward bid-ask spread is closest to:

A. 0.000251.

B. 0.0008.

C. 0.001051.

D. 0.006685.

Practice Questions: Q1 Answer

Explanation: C is correct.

The spot bid-ask spread is 0.0008 (= 1.2952 – 1.2944).

The three-month forward bid quote is: 1.2944 + 0.005634 = 1.300034, and the three-month forward ask quote is: 1.2952 + 0.005885 = 1.301085.

The forward bid-ask spread is: 1.301085 –1.300034 = 0.001051.

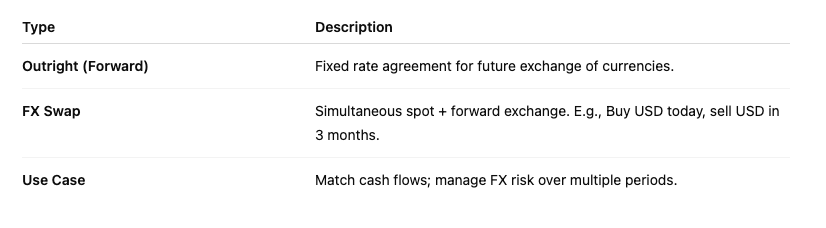

Topic 2. Outright (Forward) and Swap Transactions

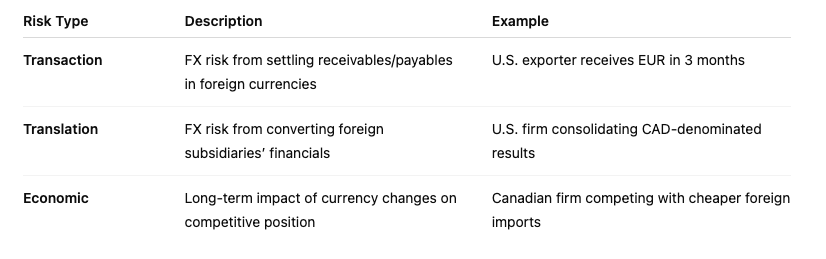

Topic 3. Transaction, Translation, and Economic Risk

Practice Questions: Q2

Q2. A multinational firm faces various risks, and it attempts to mitigate such risks with hedging techniques. Which type of risk would the firm find the most challenging to hedge?

A. Economic risk.

B. Financial risk.

C. Transaction risk.

D. Translation risk.

Practice Questions: Q2 Answer

Explanation: A is correct.

Transaction risk can be hedged with forward transactions, and translation risk can be hedged by financing assets with liabilities in the same currency. Economic is much more challenging to determine than transaction or translation risk, therefore, it is the most challenging risk to hedge.

Topic 4. Multicurrency Hedging

-

Portfolio Diversification: Currency movements < +1 correlation.

-

Forward Contracts: Lock-in rate, remove all upside/downside.

-

Options:

-

Provide downside protection, retain upside potential.

-

Use basket options or Asian options to reduce cost.

-

Module 2. Interest Rates, Inflation and Exchange Rates

Topic 1. Exchange Rate Drivers

Topic 2. Currency Appreciation/Depreciation

Topic 3. Purchasing Power Parity

Topic 4. Nominal and Real Interest Rates

Topic 5. Interest Rate Parity

Topic 1. Exchange Rate Drivers

-

Trade Flows:

-

More exports → Currency appreciates.

-

More imports → Currency depreciates.

-

-

Monetary Policy:

-

Loose policy → Currency depreciation (more supply).

-

-

Inflation:

-

Higher inflation → Currency depreciation.

-

Topic 2. Currency Appreciation/ Depreciation

Example: EURUSD moves from 1.1500 to 1.1300

-

Euro depreciates:

-

-

USD appreciates:

-

- Appreciation ≠ Equal in % terms to depreciation (due to inverse relationship)

Practice Questions: Q4

Q4. Assume the CADJPY exchange rate has changed from CADJPY 82.4012 to 83.9912. The percentage change in the JPY price of a CAD is closest to:

A. −1.89%.

B. +1.89%.

C. −1.93%.

D. +1.93%.

Practice Questions: Q4 Answer

Explanation: D is correct.

The percentage change in the JPY price of a CAD is:

(83.9912 / 82.4012) − 1 = +0.0193 = +1.93%

Because the JPY price of a CAD has risen, the CAD has appreciated relative to the JPY, and a CAD now buys 1.93% more JPY. The CAD has appreciated by 1.93% relative to the JPY.

Topic 3. Purchasing Power Parity

-

Theory: FX changes = Inflation differential

-

Example:

-

Europe inflation = 2%, U.S. = 1%

-

EURUSD current = 1.1500 → Expected = 1.1500 × 0.99 = 1.1385

-

Topic 4. Nominal and Real Interest Rates

-

Nominal Rate (r):

- Fisher Equation:

-

High real rates → Capital inflows → Currency appreciation.

-

High inflation → Imports rise → Currency depreciation.

Practice Questions: Q5

Q5. The real interest rate in Country Z is 3% and expected inflation is 50%. The nominal interest rate is closest to:

A. 47%.

B. 53%.

C. 55%.

D. 95%.

Practice Questions: Q5 Answer

Explanation: C is correct.

Nominal interest rate = [(1.03)(1.50) − 1] = 54.5%

Topic 5. Interest Rate Parity

-

Covered IRP:

-

- Ensures no arbitrage between countries' rates via forward FX.

-

Uncovered IRP: Forward = Expected future spot; no forward contract use

Practice Questions: Q5

Q5. The annual interest rate is 3% in the United States and 7% in Mexico. The spot rate for the Mexican peso is USDMXN 20. The six-month arbitrage-free forward rate is closest to:

A. USDMXN 19.25.

B. USDMXN 19.62.

C. USDMXN 20.38.

D. USDMXN 20.78.

Practice Questions: Q5 Answer

C is correct.